When a parent hands over £50,000 to help their child buy a first home, everyone is smiling. When that child’s relationship breaks down three years later, or when the parent needs the money back for care home fees, the smiles vanish — and the question that should have been answered on day one suddenly becomes the most expensive question in the room: was it a gift or a loan?

Getting this wrong doesn’t just cause family arguments. It determines how assets are divided on divorce, whether HMRC charges Capital Gains Tax or Inheritance Tax, whether a mortgage lender treats the sum as undisclosed debt, and whether a creditor in bankruptcy can claw the money back. The UK courts have developed a clear (and often brutal) framework for resolving these disputes, and understanding it now could save you tens of thousands of pounds later.

Why the Distinction Matters So Much

A gift is an outright transfer of value with no expectation of return. Once given, the donor has no legal claim to the money. A loan creates a debtor-creditor relationship: the recipient is obliged to repay, and the lender can enforce that obligation through the courts. The consequences ripple outwards:

- Divorce proceedings: Under the Matrimonial Causes Act 1973, the court must consider all financial resources and obligations. A genuine loan to one spouse is a liability that reduces the matrimonial pot. A gift is simply part of the pot to be divided. The difference can shift the settlement by the full amount transferred.

- Inheritance Tax: If a parent gives money as a gift and dies within seven years, it may be caught by the seven-year rule and subject to IHT taper relief or full liability. A loan that remains outstanding at death forms part of the deceased’s estate as a debt owed to them — a fundamentally different tax treatment.

- Mortgage applications: Lenders require gifted deposits to be confirmed as non-repayable via a gifted deposit letter. If the money is actually a loan, the applicant has undisclosed debt, the lender’s affordability assessment is wrong, and the mortgage may be voidable for misrepresentation.

- Insolvency: Under sections 339 and 423 of the Insolvency Act 1986, a trustee in bankruptcy can challenge transactions at an undervalue (gifts) made within certain time limits to recover funds for creditors.

How UK Courts Actually Decide

English and Welsh courts apply an objective test rooted in contract law principles. The leading authority remains Seldon v Davidson [1968], which established that where money is advanced between family members, there is a rebuttable presumption of a gift — unless the person claiming it was a loan can prove otherwise on the balance of probabilities. This is the opposite of what most people assume. If your mother lent you £80,000 and you both “knew” it was a loan, the court will presume it was a gift unless compelling evidence says otherwise.

More recently, in Akhmedova v Akhmedov and various reported ancillary relief cases, courts have scrutinised the following factors:

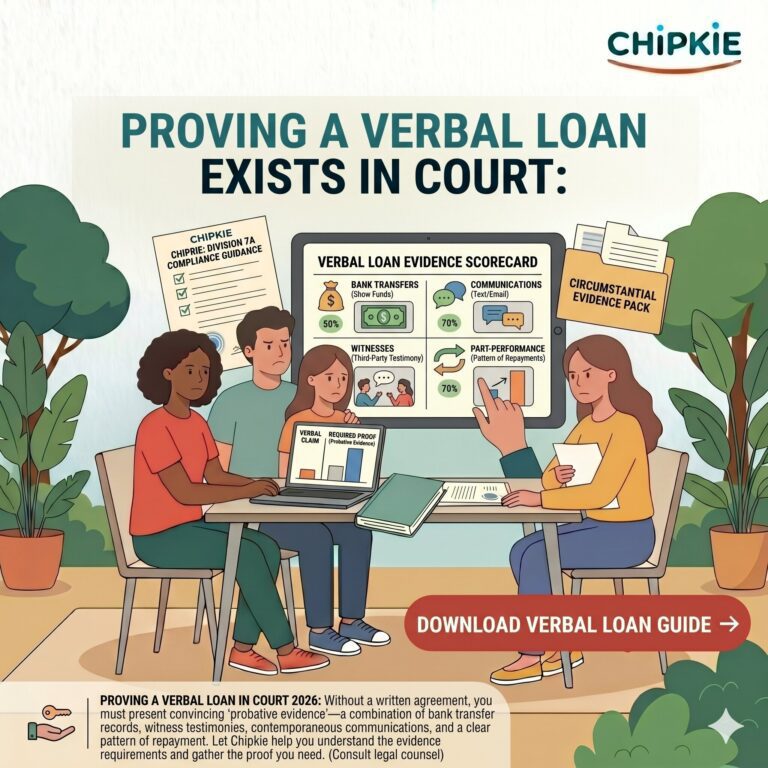

- Written documentation: A signed loan agreement is the single most persuasive piece of evidence. Without it, you are fighting uphill.

- Repayment terms: Did the parties agree a repayment schedule, interest rate, or maturity date? The absence of any repayment structure strongly suggests a gift.

- Actual repayment conduct: Even without a written agreement, evidence that the recipient made regular repayments — traceable through bank statements — can rebut the presumption of a gift. Conversely, years of silence followed by a sudden demand for repayment at the point of divorce looks deeply suspicious to a judge.

- Contemporaneous communications: Text messages, emails, or WhatsApp conversations at or around the time of the transfer carry enormous weight. A message saying “here’s some money to help you get started, no need to pay it back” is devastating to a subsequent loan claim.

- The context and occasion: Money transferred at Christmas, on a wedding day, or as a graduation present will be presumed a gift far more readily than money transferred alongside a spreadsheet of repayment dates.

- Tax returns and accounts: If the lender never declared the loan as an asset, or the borrower never disclosed it as a liability, the court will question whether either party truly treated it as a loan at the time.

The Presumption of Advancement — and Its Limits

Historically, the equitable presumption of advancement meant that transfers from parent to child, or from husband to wife, were automatically presumed to be gifts. Section 199 of the Equality Act 2010 was intended to abolish this presumption, but that section has never been brought into force. The presumption therefore technically still applies, though modern courts give it little independent weight. What matters far more is the totality of the evidence. Do not rely on old equitable doctrines — rely on paperwork.

The Deed Question: Six Years or Twelve?

Under the Limitation Act 1980, a claim on a simple contract (including an informal loan agreement) must be brought within six years of the cause of action arising — typically the date repayment was due. However, if the loan agreement is executed as a deed, the limitation period extends to twelve years. For family loans that may not be called in for many years, this distinction is critical. A deed requires specific formalities: it must be in writing, stated to be a deed, signed, witnessed, and delivered. The cost of having a solicitor prepare one is modest; the protection it provides is substantial.

What Happens in Divorce Specifically

Family courts apply section 25 of the Matrimonial Causes Act 1973, which requires consideration of all the circumstances. Judges are acutely aware that parents sometimes “discover” that a gift was actually a loan once their child’s marriage collapses, hoping to extract the money before the other spouse can claim a share. The court in Hammond v Mitchell [1991] and numerous subsequent cases has shown willingness to look behind self-serving assertions. If the evidence is equivocal, the court will almost always classify the transfer as a gift — and divide it accordingly. The parent loses everything.

Protecting Yourself: What You Should Actually Do

Whether you are lending or borrowing, giving or receiving, the following steps are non-negotiable if you want certainty:

- Put it in writing at the time of the transfer. A loan agreement should specify the amount, purpose, repayment terms (including any interest), what happens on default, and whether the loan is secured against any asset. Sign it as a deed for the twelve-year limitation period.

- If it is genuinely a gift, confirm that in writing too. A short letter stating the money is an unconditional gift protects both parties — especially the recipient, who may later face claims from the donor’s other family members or creditors.

- Make repayments from a traceable account. Standing orders from a named bank account, with clear references, create an audit trail no court can ignore.

- Declare the arrangement properly. Lenders must be told about loans affecting deposit sources. Tax returns should reflect interest received or debts owed. Consistency across all records is what persuades a judge.

- Review the arrangement when circumstances change. Marriage, divorce, death, insolvency, or a property sale should all trigger a review of whether the loan terms need updating or the debt needs calling in.

- Take legal advice before transferring significant sums. A thirty-minute consultation with a solicitor before transferring £50,000 is infinitely cheaper than a three-day hearing to determine what it was afterwards.

The uncomfortable truth is that family financial arrangements fail not because people are dishonest, but because they are optimistic. They assume goodwill will persist, that everyone will remember the same conversation the same way, and that formality is somehow an insult to trust. It is not. A clear written agreement is the greatest act of trust — it means both parties are confident enough in their intentions to commit them to paper. Do it now, while everyone is still smiling.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered financial or legal advice. Property and lending laws in the United Kingdom vary and may change over time. We always recommend consulting with a qualified solicitor and mortgage broker before entering into a property purchase or financial arrangement with another party.