With household budgets squeezed by rising energy tariffs, council tax hikes, and stubborn food inflation, more British families are turning to each other for financial support. Cost of living borrowing from family 2026 is no longer a last resort — it has become a mainstream strategy. Research from the Money and Pensions Service suggests that millions of UK adults now rely on informal family loans to bridge gaps between paydays or fund essential purchases. But while borrowing from a relative can be faster, cheaper, and less stressful than applying for commercial credit, it comes with risks that most people dramatically underestimate.

Done well, a family loan can save you hundreds in interest and preserve your credit file. Done badly, it can fracture relationships, trigger unexpected tax liabilities, and leave both parties legally exposed. This guide walks you through the practical, legal, and emotional dimensions you need to consider before asking — or agreeing — in 2026.

Why is cost of living borrowing from family surging in 2026?

Persistently high living costs, elevated interest rates, and tighter lending criteria are pushing more UK households toward family borrowing. The Bank of England base rate remains above historical norms, making personal loans and credit cards expensive. Family lending fills the gap — an estimated one in four British adults has either lent to or borrowed from a relative in the past twelve months.

- Energy bills: Ofgem’s price cap adjustments continue to outstrip wage growth for many households, particularly renters and those on prepayment meters.

- Mortgage renewals: Borrowers rolling off low fixed rates face payment shocks of £200–£400 per month, often prompting a request to parents for bridging support.

- Childcare costs: Even with the expanded 30-hour free childcare offer, nursery top-ups and wraparound care eat into disposable income.

- Credit tightening: The Financial Conduct Authority reports that lenders are applying stricter affordability checks, leaving some applicants — especially self-employed workers — unable to access mainstream credit.

The result is a growing reliance on the so-called “Bank of Mum and Dad,” though in 2026 it extends well beyond parents helping with house deposits. Siblings, grandparents, aunts, and uncles are all stepping in. As we explored in our article on how British families are pooling resources across generations, this trend has deepened significantly over the past year.

What are the hidden risks of borrowing from family during the cost of living crisis?

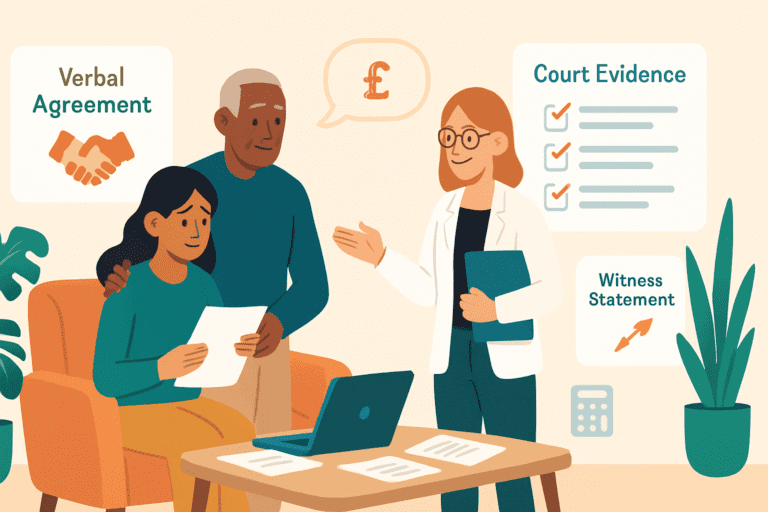

Family loans feel low-risk because there is no credit check and no formal application. However, they carry legal, tax, and relationship risks that commercial borrowing does not. Without a written agreement, disputes over whether money was a loan or a gift are the single most common cause of family financial litigation in England and Wales.

Could HMRC treat a family loan as a taxable gift?

Yes. If there is no documentation proving a loan exists — including repayment terms and any interest — HMRC may treat the transfer as a gift. If the lender dies within seven years, the amount could fall into their estate for Inheritance Tax purposes, potentially triggering a 40% liability above the nil-rate band.

This is a trap families consistently fall into. A parent lending £30,000 to help a child cover eighteen months of mortgage shortfalls may never think about IHT. But without a signed loan agreement, the executors of the estate — and HMRC — may classify the sum as a potentially exempt transfer. Our detailed guide on UK Inheritance Tax 2026 relief caps explains the current thresholds and how to stay compliant.

What happens if there is no written agreement?

Without a written agreement, the borrower and lender rely entirely on memory and goodwill. UK courts regularly hear cases under contract law where one party claims the money was a gift and the other insists it was a loan. The burden of proof falls on the person claiming it was a loan — and text messages alone are often insufficient evidence.

- Record the amount, date, and purpose of the loan in writing.

- Agree a repayment schedule — even if it is informal, put it on paper.

- State whether interest applies. A zero-interest loan is perfectly legal, but you should say so explicitly.

- Sign the document. Consider executing it as a deed for the 12-year limitation period rather than the 6-year period for a simple contract.

- Keep copies — both parties should retain signed originals or certified digital copies.

For a step-by-step walkthrough, see our guide on how to write a loan agreement between family or friends in the UK.

Can a family loan affect your mortgage application?

Absolutely. Mortgage lenders require full disclosure of all debts, including family loans. An undeclared family loan discovered during underwriting can result in an application being declined or, worse, flagged as mortgage fraud. Lenders stress-test total debt commitments, so even an interest-free family loan reduces your borrowing capacity.

If the loan is genuinely a gift — for example, a parent giving money toward a deposit — most lenders require a signed gifted deposit letter confirming no repayment is expected. Misrepresenting a loan as a gift is a criminal offence under the Fraud Act 2006.

How can families structure cost of living loans to protect everyone?

A well-structured family loan protects the relationship, satisfies HMRC, and gives both parties legal certainty. Here is a practical framework based on what we consistently see working across the agreements our users create:

| Element | Why it matters | Example |

|---|---|---|

| Loan amount | Clarity prevents disputes | £5,000 transferred on 15 March 2026 |

| Repayment schedule | Sets expectations for both sides | £250/month for 20 months, starting 1 May 2026 |

| Interest rate | HMRC compliance; fairness | 0% (stated explicitly) or 2% simple interest |

| Early repayment clause | Flexibility if borrower’s finances improve | Borrower may repay in full at any time without penalty |

| Default provisions | Protects lender; avoids escalation | 30-day grace period, then mediation before legal action |

| Signed as deed or contract | Limitation period (12 vs 6 years) | Deed recommended for amounts above £5,000 |

Communication is as important as documentation. Agree upfront what happens if the borrower cannot make a payment. Will there be a pause? Will the term extend? Addressing these scenarios before they arise prevents the awkward conversations that destroy family trust.

What should you consider before asking family for money in 2026?

Before approaching a relative, run through this honest self-assessment. Cost of living borrowing from family in 2026 should be a considered decision, not an impulsive one.

- Have you exhausted other options? Check eligibility for government support via MoneyHelper, including council tax reduction, Universal Credit top-ups, or the Household Support Fund.

- Can you genuinely repay? If your budget cannot absorb the repayments, you risk compounding your financial stress and damaging the relationship.

- Is the lender financially stable? Lending money they cannot afford to lose puts both parties at risk. A parent drawing down savings earmarked for retirement to help an adult child may create a bigger problem down the line.

- Are other family members aware? Sibling resentment over perceived favouritism is a common fallout. Transparency — within appropriate boundaries — reduces future conflict.

- Would a smaller amount solve the problem? Borrow only what you need. A £2,000 loan to cover two months of shortfall is far easier to manage than a £10,000 catch-all.

Frequently asked questions

Is cost of living borrowing from family 2026 better than using a credit card?

It depends on the terms. A zero-interest family loan is almost always cheaper than a credit card charging 20%+ APR. However, a 0% introductory credit card offer may be preferable if you can repay within the promotional period, because it avoids the relationship risk entirely and builds your credit history.

Do you need a solicitor for a family loan agreement?

Not always. For straightforward loans under £10,000, a clearly written agreement signed by both parties is usually sufficient. For larger sums — particularly those connected to property purchases — professional legal advice is strongly recommended to address tax, IHT, and potential mortgage implications.

Can a family loan affect your credit score?

A private family loan does not appear on your credit file because it is not reported to credit reference agencies. However, if the loan enables you to reduce credit card balances or avoid missed payments, it can indirectly improve your score. Conversely, undisclosed debts can cause problems during mortgage affordability assessments.

How much can you lend to a family member tax-free in the UK?

There is no limit on the amount you can lend tax-free, provided it is a genuine loan with an expectation of repayment. Interest charged above HMRC’s thresholds may be taxable as income for the lender. If the loan is later forgiven, HMRC may treat the forgiven amount as a gift for IHT purposes.

Is borrowing from family the right move for you?

Cost of living borrowing from family 2026 can be a lifeline — but only when both sides enter the arrangement with clear expectations, proper documentation, and honest communication. The financial pressure is real, and there is no shame in seeking help from people who care about you. The key is to treat the arrangement with the same rigour you would apply to any financial commitment.

Chipkie makes it simple to create, track, and manage family loan agreements digitally — so you can protect your finances and your relationships at the same time. Whether you are lending £500 to help with bills or borrowing £20,000 toward a deposit, start with a proper agreement and give everyone peace of mind.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered financial or legal advice. Property and lending laws in the United Kingdom vary and may change over time. We always recommend consulting with a qualified solicitor and mortgage broker before entering into a property purchase or financial arrangement with another party.