The Bottom Line

This definitive May 2026 Australian Federal Budget guide details a monumental structural overhaul, locking in the abolition of negative gearing for established homes, a new 30% minimum tax on discretionary trusts, and the replacement of the 50% CGT discount with indexation. For the Bank of Mum and Dad, the transition to Chalmers’ “Fourth Economy” means informal handshakes are now high-risk triggers for aggressive ATO private wealth audits and relationship breakdown losses. Navigating these changes alongside APRA’s rigid 6x debt-to-income caps requires moving away from cash gifts toward formal, legally binding loan agreements.

The delivery of the 2026-27 Australian Federal Budget marks a historic pivot in the nation’s fiscal and economic management. Serving as a blueprint for Treasurer Jim Chalmers’ “Fourth Economy,” this budget is designed to address structural intergenerational imbalances, contain inflation, and enforce “revenue repair”.

With commodity windfalls narrowing the 2025-26 deficit to $23.8 billion, the government has used its political capital not for giveaways, but to permanently dismantle long-standing tax concessions. For family investors and parents helping the next generation enter the property market, the rules of wealth transfer have been fundamentally rewritten.

1. Macroeconomic Context: The Fourth Economy Blueprint

The budget moves Australia into a defensive economic posture tailored for a global landscape defined by repeated supply-side shocks and geopolitical volatility. While sustained high prices for iron ore, metallurgical coal, and gold delivered a massive $27 billion revenue windfall over the four-year forward estimates, the long-term fiscal strategy centers on stripping back structural expenditures.

Fiscal Aggregate Core Targets

| Fiscal Aggregate | 2025-26 (MYEFO) | 2025-26 (Revised) | 2026-27 (Projected) | 2029-30 (Medium-Term) |

| Underlying Cash Balance | -$36.8 Billion | -$23.8 Billion | -$22.0 Billion | Narrowing Deficit |

| Commodity Revenue Boost | -$27.0 Billion | — | — | — |

| Structural Savings (NDIS) | — | $25.0 Billion | $35.0 Billion | $170.0 Billion |

| Net Policy Decisions | — | — | -$2.0 Billion | Net Save |

The multi-billion dollar structural savings pulled from the National Disability Insurance Scheme (NDIS)—curbing annual growth from 10% to 2% to save $170 billion over a decade—will directly fund domestic energy security, national defense, and highly targeted cost-of-living relief.

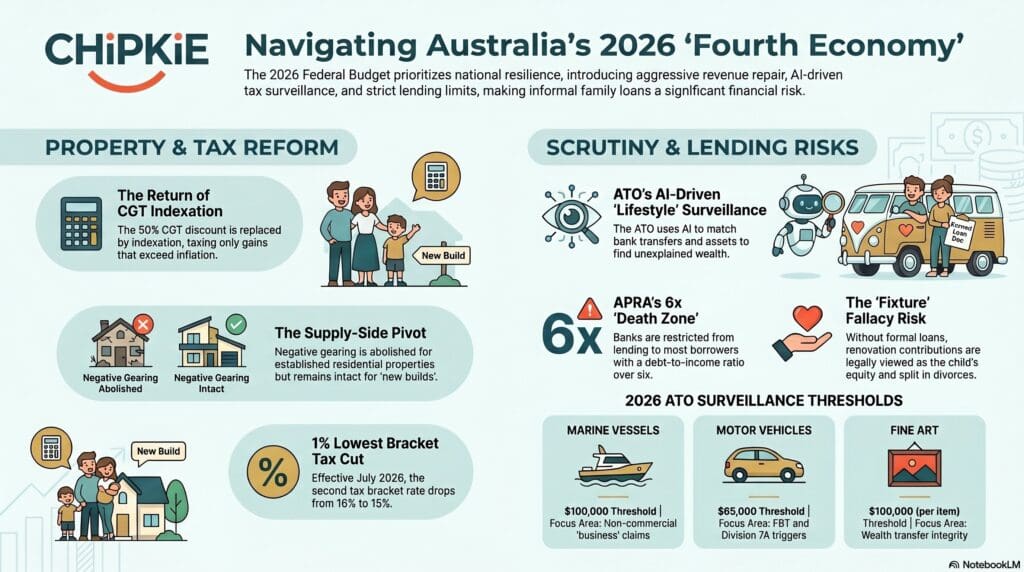

2. Property Overhaul: The Death of the 50% CGT Discount

The most significant structural disruption in the budget is the complete elimination of the 50% Capital Gains Tax (CGT) discount, replaced effective 1 July 2027 by a cost base CPI indexation model combined with a new 30% minimum tax on net capital gains.

Under the old rules, individuals were only taxed on half their nominal capital gains for assets held longer than 12 months. From 1 July 2027, the cost base of the asset will instead be adjusted in line with the Consumer Price Index (CPI), ensuring that only real gains—those exceeding inflation—are subject to tax at the individual’s marginal rate.

The 30% Minimum Tax Floor

The introduction of the 30% minimum tax establishes a floor for the tax payable on capital gains, primarily impacting taxpayers whose effective marginal tax rate is less than 30%. Most notably, pre-1985 “pre-CGT” assets lose their blanket exemption. Capital gains accruing on these historical assets after 1 July 2027 will now be drawn into the new indexation and 30% minimum tax net.

Straddle Assets & The Valuation Deadline Danger

For assets held prior to 1 July 2027 but sold after that date, the 50% CGT discount will continue to apply to gains accrued up to 1 July 2027. Taxpayers have two specific methods to determine this split:

- Method 1 (Market Valuation): Obtain a formal independent registered valuation of the asset as of 1 July 2027. This value forms the new cost base for the indexation phase.

- Method 2 (Specified Apportionment Formula): Rely on a default ATO mathematical formula that estimates the 1 July 2027 value based on the growth rate over the entire holding period.

Strategic Play: Property advisors strongly recommend commissioning a registered property valuation before 1 July 2027. Relying on the ATO’s default apportionment formula risks significantly understating the property’s true market value at the boundary line, which can cost investors tens of thousands of dollars in unnecessary top-up tax upon disposal.

3. Negative Gearing Abolished for Established Dwellings

Negative gearing has been completely abolished for all established residential properties purchased after 7:30pm AEST on 12 May 2026 (contract date), with the operational changes taking effect from 1 July 2027.

Affected property investors will no longer be allowed to offset net rental losses against their salary or other personal income. Instead, net rental losses can only be offset against residential rental income (including from other properties) or future capital gains from rental properties, with excess losses carried forward indefinitely.

Grandfathering and the New Build Exemption

- Existing Property Owners: Properties under contract or held prior to 7:30pm on 12 May 2026 are fully grandfathered and can continue negatively gearing under current rules until sold.

- The New Build Carve-Out: To protect the pipeline of housing construction, eligible new builds are completely exempt. Investors in new residential properties retain full access to negative gearing. Furthermore, upon disposal, they are granted a unique choice: they can select either the traditional 50% CGT discount or the new indexation and 30% minimum tax regime.

4. Trust Reform: The 30% Discretionary Trust Minimum Tax

To combat the use of family trusts for aggressive tax planning and income splitting, the government has introduced a flat 30% minimum tax on discretionary trusts starting 1 July 2028.

Trustees will be required to pay tax at a minimum rate of 30% on the taxable income of the trust. This neutralizes the tax arbitrage benefit of distributing income to low-marginal-rate individual beneficiaries (such as adult children) or utilizing 30% “bucket” corporate entities. Beneficiaries (other than companies) will receive non-refundable tax credits for the tax paid by the trustee.

To mitigate the shock of this massive structural shift, the government is providing an expanded three-year rollover relief window starting 1 July 2027 to support small businesses and families wishing to restructure out of discretionary trusts into other entity types without triggering immediate tax events.

5. ATO Integrity Priorities and Expanded Data Matching

The Australian Taxation Office (ATO) has been handed an increasingly data-driven mandate for the 2026-27 financial year, backed by real-time automated matching. The gap between what the ATO knows and what taxpayers declare has evaporated.

ATO 2026 Compliance Matrix

| Compliance Focus | Key ATO Risk Factor | Consequence of Non-Compliance |

| Discretionary Trusts | Income splitting & Section 100A breaches | Assessment of the top marginal tax rate |

| Trust Minimum Tax | Circulating trust-to-trust distributions | Breach of the 30% minimum tax threshold |

| Division 7A | Shareholder “loans” lacking written agreements | Amount taxed as unfranked dividend (up to 47%) |

| Lifestyle Assets | Corporate-owned vehicles/boats used for private hobbies | FBT and Division 7A tax triggers |

| Crypto & CARF | Unreported international exchange transactions | Automated audit and Shortfall Interest Charge |

For private companies, the Division 7A benchmark interest rate is locked at 8.37%. All loans from a private company to shareholders or associates must be governed by compliant, written agreements with minimum yearly repayments made at this rate to avoid the principal being treated as a taxable unfranked dividend.

6. APRA’s 6x Debt-to-Income “Speed Limit”

The 2026 property market operates under tight macroprudential settings designed to contain systemic risk as interest rates stabilize around a cash rate of 4.35%. Authorised deposit-taking institutions (ADIs) are strictly restricted to lending no more than 20% of new mortgages to borrowers with a debt-to-income (DTI) ratio of six or more.

$$\text{DTI Ratio} = \frac{\text{Total Debt}}{\text{Gross Annual Income}}$$

This limit is applied independently to owner-occupier and investor portfolios on a quarterly basis. Notably, bridging loans and loans for the purchase or construction of new dwellings are exempt from this DTI cap to encourage new supply. Navigating these rigid DTI limits is a mechanical necessity for any family lender trying to help a child pass bank serviceability metrics.

7. HECS-HELP Debt Reform & Income Tax Cuts

To offset the bite of these investment property rollbacks, the budget solidifies substantial cost-of-living relief targeting low- and middle-income earners:

- HECS-HELP Reform: Confirms the transition of student loans to a “marginal repayment system” effective 1 July 2026. Compulsory repayments are calculated only on the portion of income above the new $67,000 threshold (up from $54,435), rather than on total income. Paired with indexation capped at the lower of the Wage Price Index (WPI) or CPI, this immediately lowers PAYG withholding and boosts graduate borrowing capacity. If your child is struggling with the HECS debt impact on a mortgage application, their position just improved significantly.

- Income Tax Rate Cuts: Effective 1 July 2026, the tax rate for the second bracket ($18,201 to $45,000) decreases from 16% to 15%, dropping further to 14% on 1 July 2027.

- Standard $1,000 Deduction: Wage earners can claim a flat $1,000 work deduction from 1 July 2026 without itemizing costs or retaining receipts.

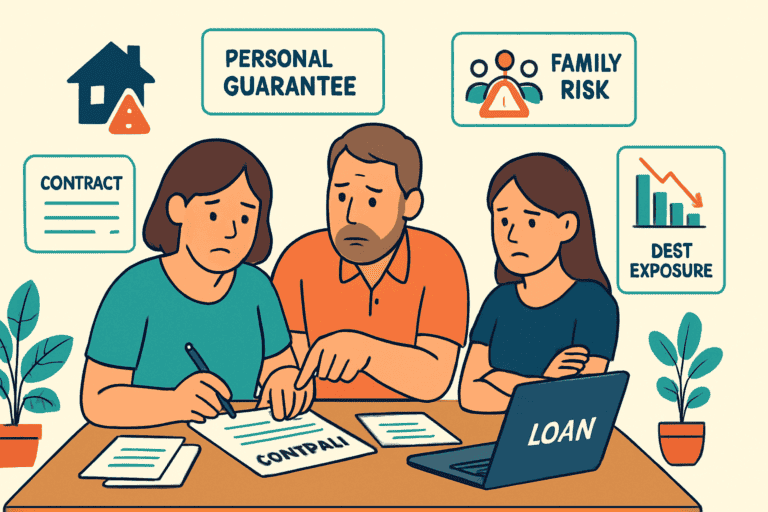

8. The “Bank of Mum and Dad,” Succession, and the Hotchpot Rule

With Australian parents contributing an estimated $35 billion annually to help their children enter the housing market, intergenerational wealth transfer has become a highly litigated legal arena. Recent surveys show that 34% of Australians require help from the “Bank of Mum and Dad” to buy a home.

With discretionary trusts facing a 30% tax floor and established property negative gearing abolished, families are moving away from informal cash gifts. Without a formal, written loan agreement executed at the time funds are advanced, family law courts will typically treat parental assistance as an unconditional gift.

Informal Cash Gift / Undocumented Loan

│

┌────────────────────────┴────────────────────────┐

▼ ▼

Family Law Court ATO Audit

(Relationship Breakdown) (Division 7A / FBT)

│ │

Treated as a Gift; Deemed Dividends;

absorbed into the asset pool unfranked top-up tax

and split with ex-partner at rates up to 47%

The Fragmented Doctrine of Hotchpot

The Hotchpot Rule requires an estate’s personal representative to take into account lifetime gifts or advancements made to children when calculating their final share of an estate. Its application across Australia is highly fragmented:

- ACT, South Australia, and Northern Territory: The Hotchpot rule actively applies to intestate estates.

- NSW, QLD, WA, TAS, and VIC: The doctrine of Hotchpot has been completely abolished for intestate estates.

Even in states where intestacy laws have abolished Hotchpot, testators frequently insert custom Hotchpot or Equalisation clauses into their Wills to ensure fairness. To prevent relationship breakdowns from absorbing family capital and avoid structural estate traps, families must move from handshakes to secured private credit.

9. Synthesis: The May 2026 Budget Cheat Sheet

| Sector | Key Budget Rule / Change | Professional Strategy |

| Housing (Established) | Negative gearing abolished for purchases post-12 May 2026 | Transition portfolio focus to new builds or cash-flow positive assets. |

| Housing (New Builds) | Exempt from negative gearing cuts; choice of CGT regimes | Optimize acquisitions of off-the-plan properties to access dual CGT pathways. |

| CGT (All Assets) | 50% discount replaced by CPI indexation & 30% minimum tax | Obtain registered property valuations before 1 July 2027 to lock in pre-reform gains. |

| Discretionary Trusts | 30% minimum tax rate from 1 July 2028 | Utilize 3-year rollover relief to restructure into corporate or partnership entities. |

| Lending | APRA 6x DTI Limits | Structure family capital as a formal loan to preserve divorce protection and clear bank hurdles. |

How Chipkie Supports Your 2026 Strategy

The transition to Chalmers’ Fourth Economy proves that undocumented family financing is a critical compliance liability. Between the ATO’s automated data-matching network tracking private wealth transfers and the family court’s default treatment of informal gifts, an unrecorded handshake is a structural risk.

Chipkie provides the digital infrastructure to transform your family’s financial backing into a compliant, legally binding loan agreement. By automating contract generation, factoring in local compliance requirements, and generating a transparent repayment trail, we ensure your capital remains recognized as a legitimate debt liability, protecting it from tax office reclassification and securing it against unexpected relationship breakdowns. Don’t let your intergenerational generosity become an audit statistic.

Disclaimer: Chipkie is a financial technology provider and does not offer legal, tax, or financial advice. This May 2026 Australian Federal Budget guide is for informational purposes only. Always consult a qualified solicitor or registered tax agent to understand how these structural budget overhauls impact your specific tax obligations, company structures, and estate planning.

External Authority: Review the official ATO Specific Data-Matching Programs for 2026 at ATO.gov.au.