Financial Boundaries Family: 7 Rules That Work

Protect your relationships and your wallet with these 7 proven financial boundaries family rules that stop resentment before it starts. Find out how.

Protect your relationships and your wallet with these 7 proven financial boundaries family rules that stop resentment before it starts. Find out how.

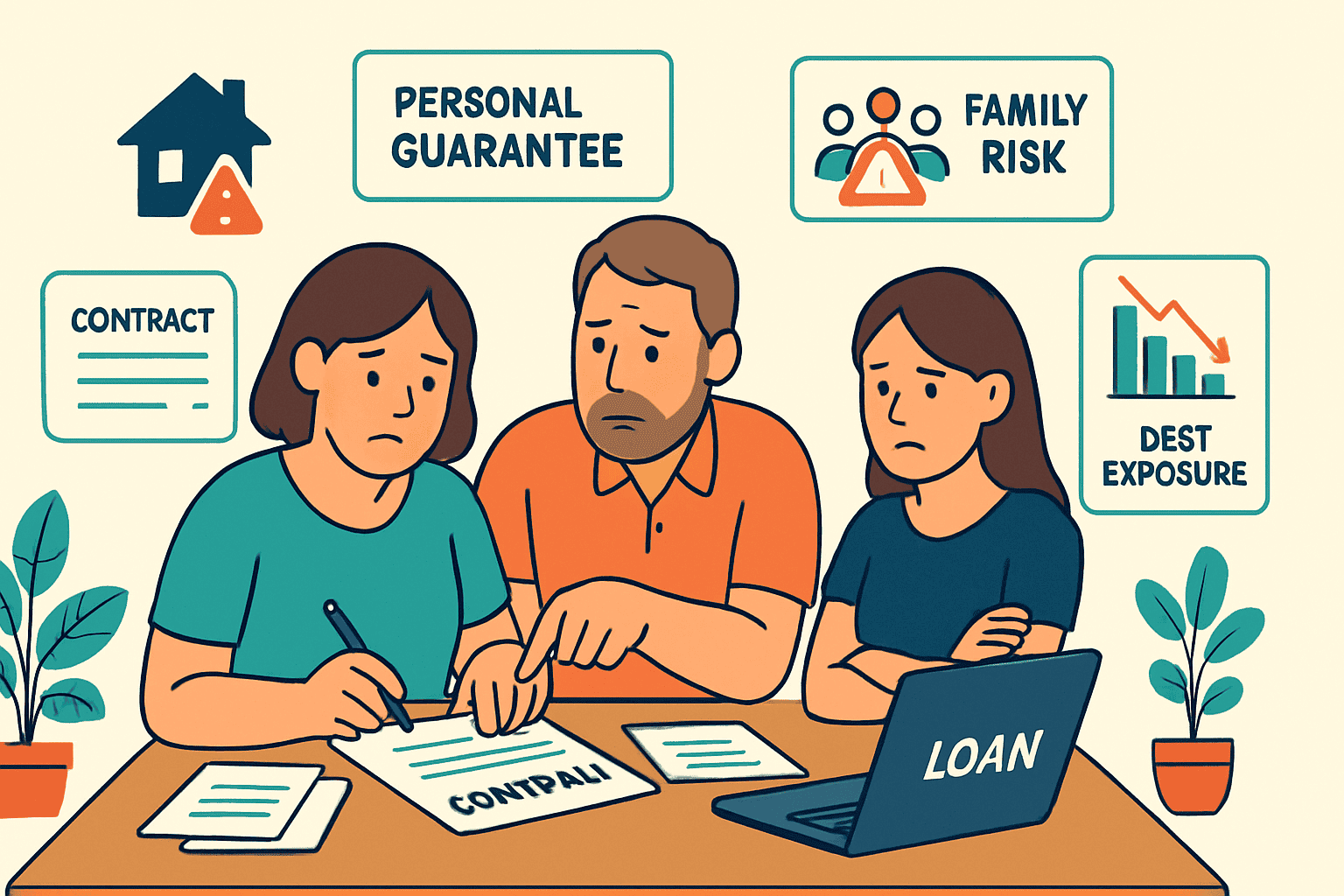

Understand the family personal guarantee risks Australians face in 2026, from hidden liabilities to asset loss, and how to protect yourself. Find out more.

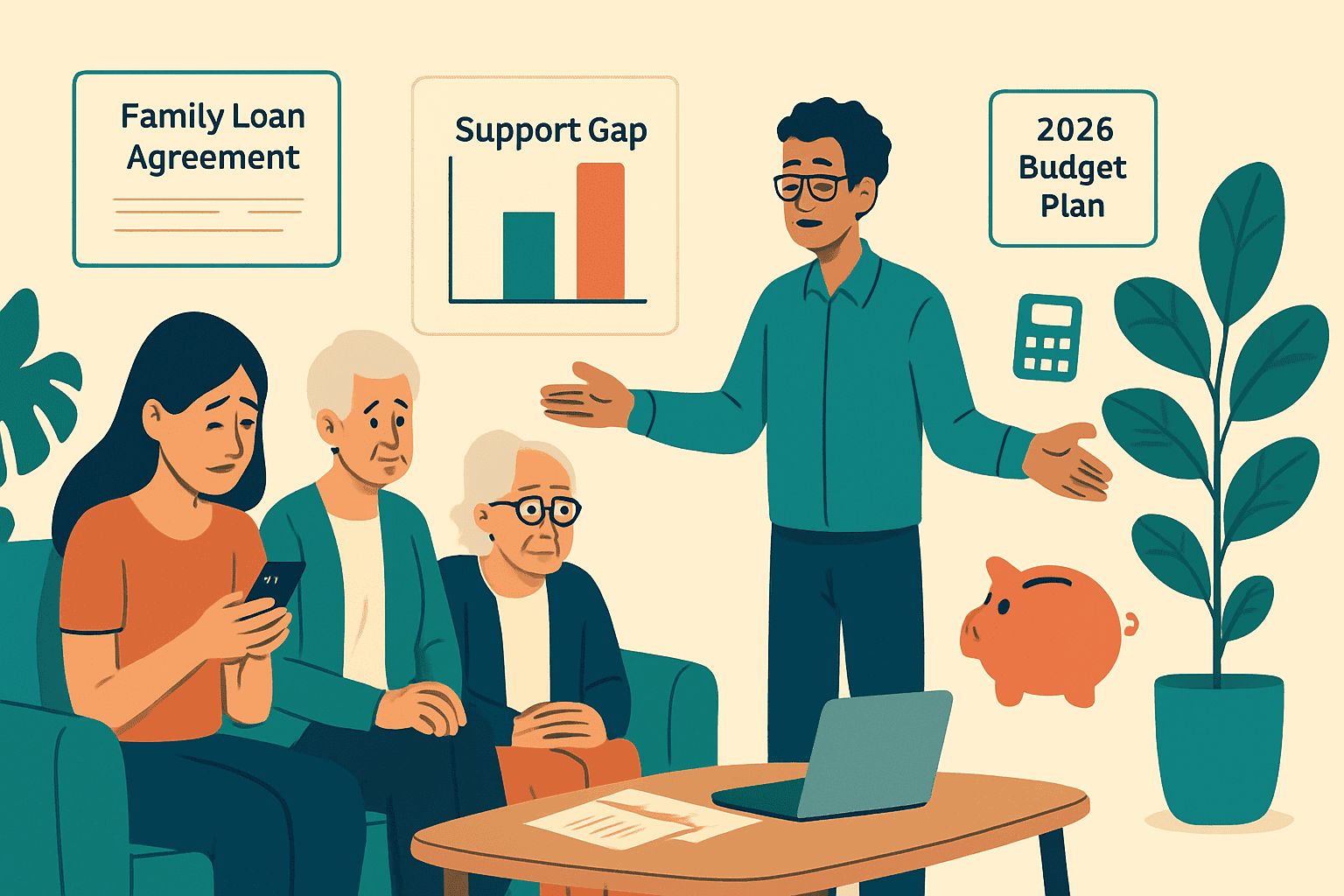

Discover how to structure a family loan for aged care in Australia, protect relationships, and navigate Centrelink rules in this 2026 guide. Find out how.

Discover whether you can use your pension for house deposit in Australia, including super access rules and key 2026 considerations. Find out how.

Discover how the family financial help gap is reshaping wealth and housing access for Australians in 2026, plus strategies to bridge it. Find out more.

Discover how a family loan for essentials can cover groceries, bills and medical costs without the pitfalls of informal arrangements. See what you need to know.

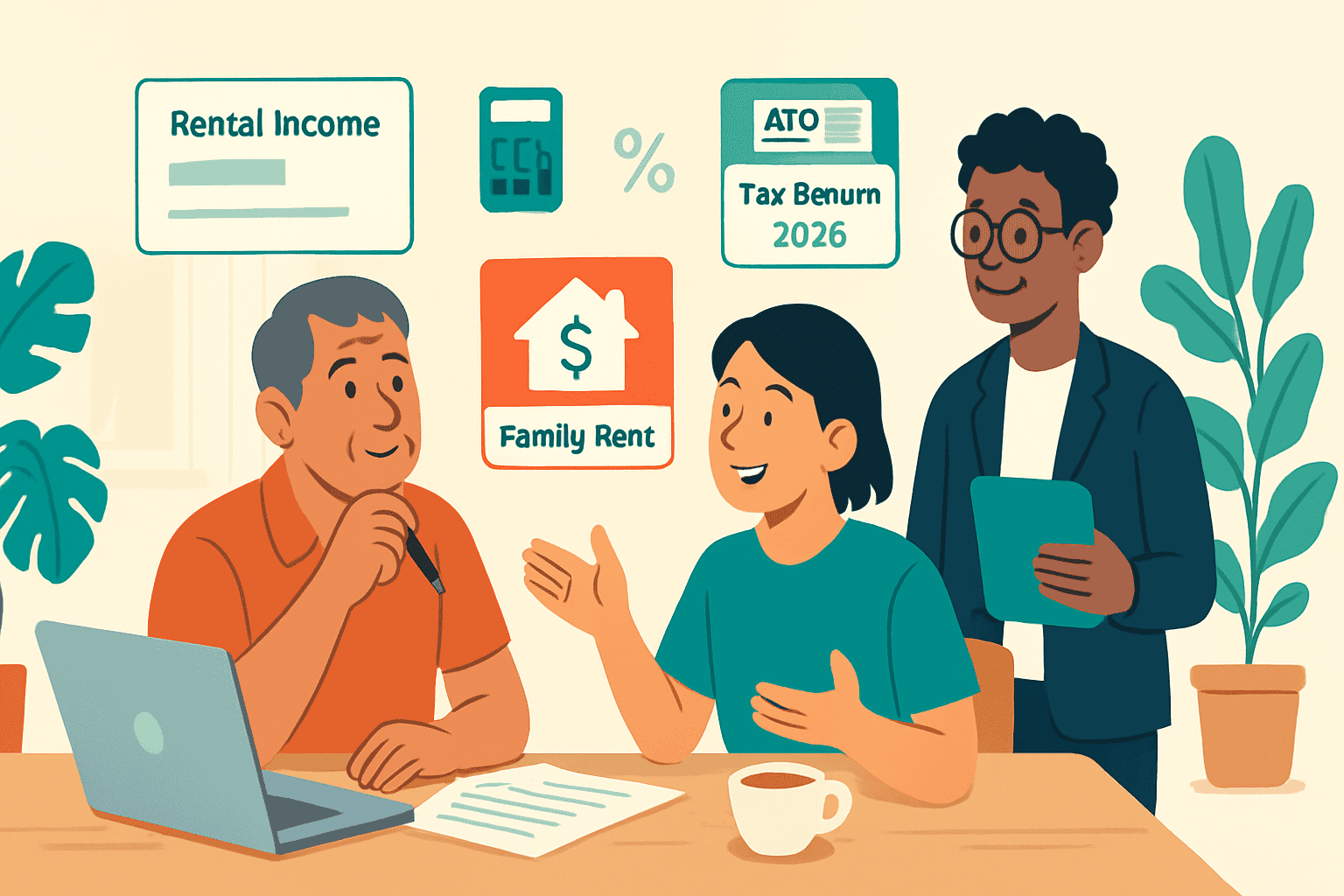

Wondering if my child pays rent is it taxable in Australia? Discover ATO rules, key thresholds, and how to avoid mistakes in this 2026 guide. Find out more.

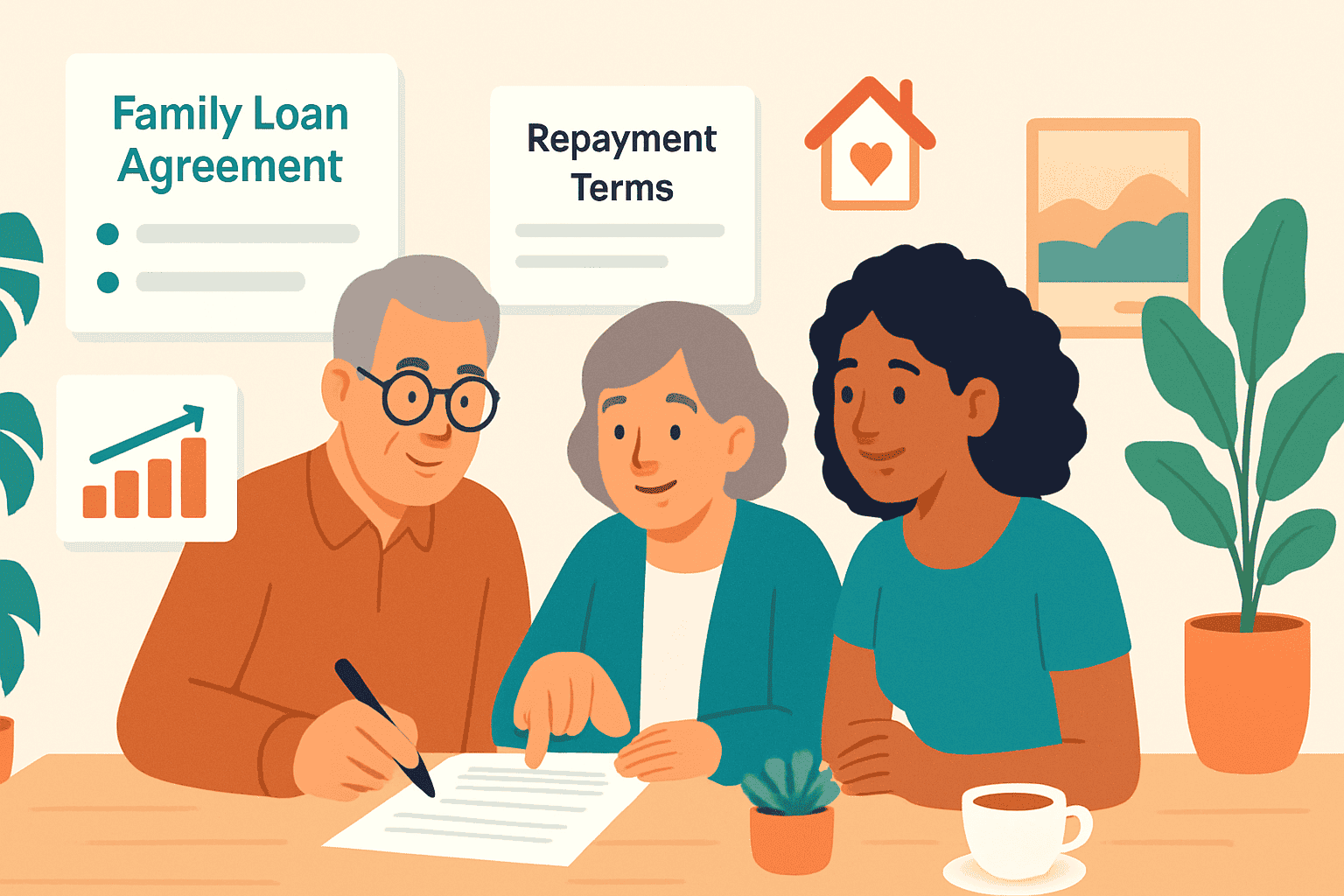

Protect your family and finances with a bank of mum and dad contract. Get essential templates, tips and legal insights for Australian families. See what you need to know.

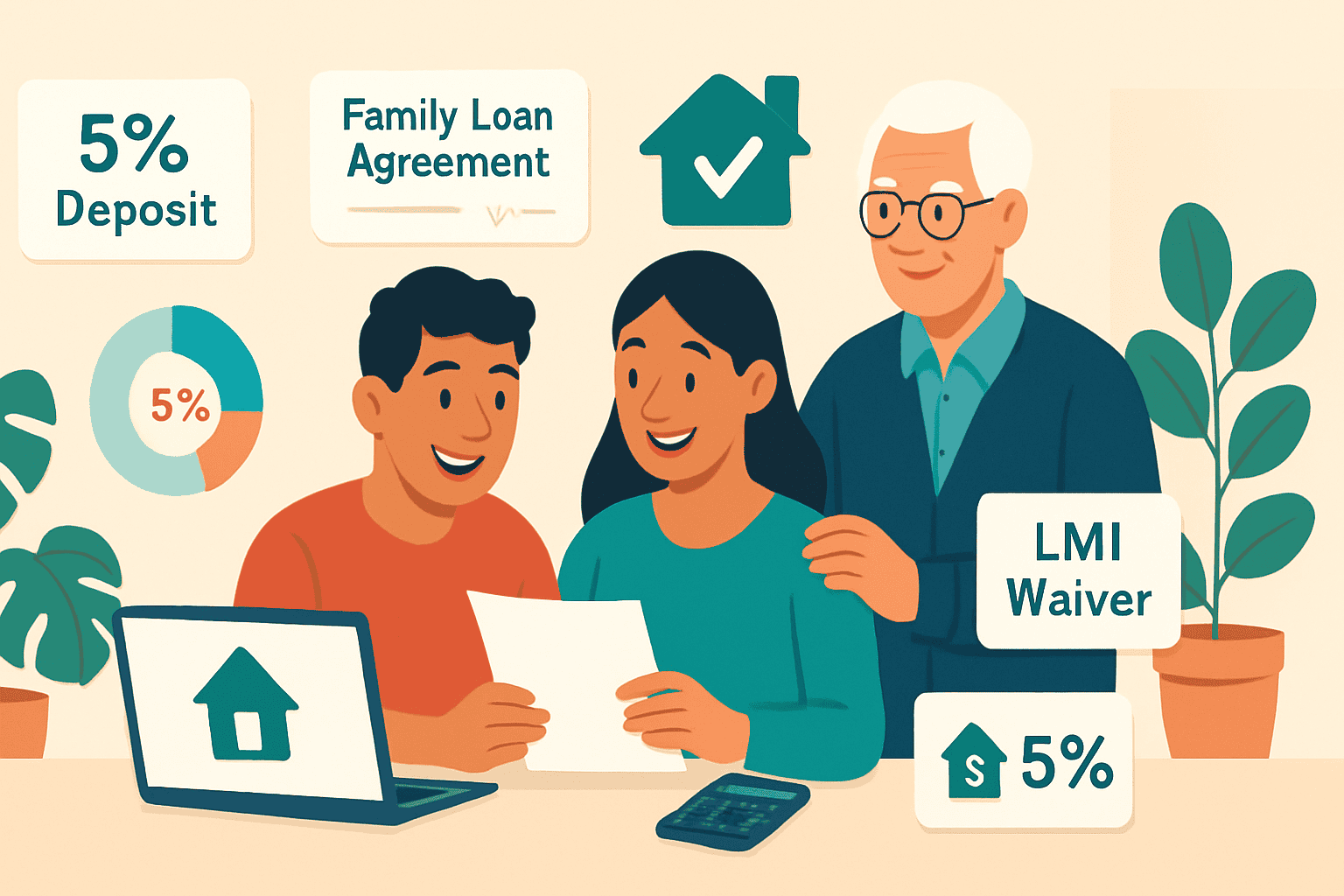

Discover how a 5% deposit scheme family loan can help you buy your first home sooner without saving a full 20% deposit. See what you need to know.

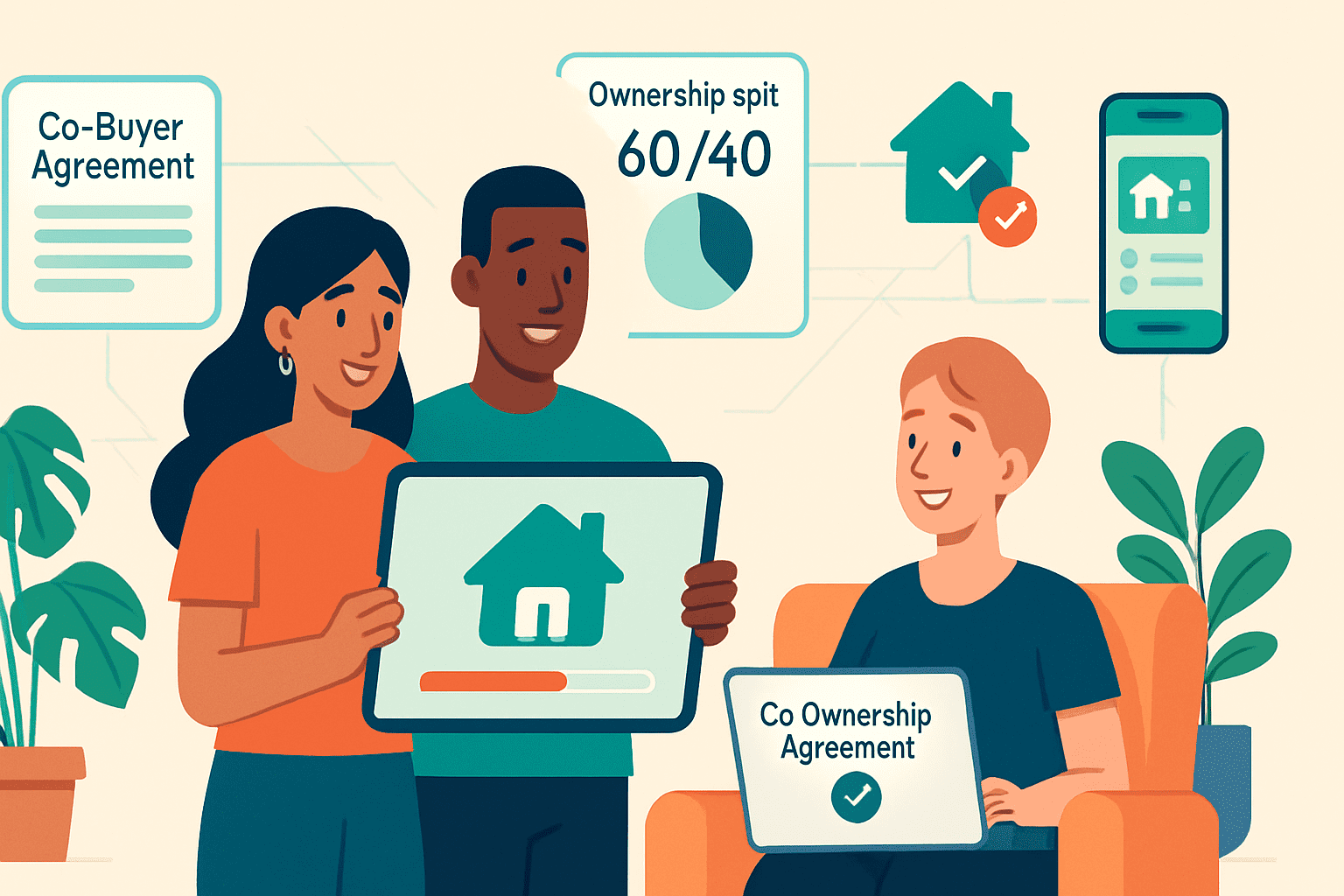

Discover how co-buying property technology helps Australians split costs, manage legal steps and get on the property ladder together in 2025. Find out how.