Family lending is woven into British life — from parents helping with house deposits to siblings bridging a gap between jobs. Yet when things go wrong, proving a verbal family loan in court becomes one of the most stressful legal challenges a person can face. Without a signed document, how do you convince a judge that the money was a loan and not a gift? English and Welsh law does allow verbal contracts, but the legal requirements for proving one are demanding, and the burden of proof falls squarely on the person claiming repayment.

This guide explains exactly what the courts look for, what evidence you need, and the practical steps that can make or break your case.

Is a verbal loan agreement legally binding in the UK?

Yes. Under English and Welsh contract law, a verbal agreement to lend and repay money is a valid, enforceable contract — provided the essential elements of a contract are present: offer, acceptance, consideration (the money itself), and an intention to create legal relations. No written document is strictly required for a simple loan between individuals.

The challenge is not legality but proof. In court, the claimant must establish, on the balance of probabilities, that the money transferred was intended as a loan rather than a gift. This is where most family claims stumble. Courts are well aware that family members routinely give each other money with no expectation of repayment, so judges apply particular scrutiny to claims that an informal transfer was actually a loan.

There is also a crucial timing point many people miss. Under the six-year limitation period for simple contracts, your right to sue expires six years from the date the money became due. If no repayment date was agreed, courts may treat the loan as repayable on demand — and the clock starts ticking from the date the demand was made. Wait too long, and you lose the right to claim entirely.

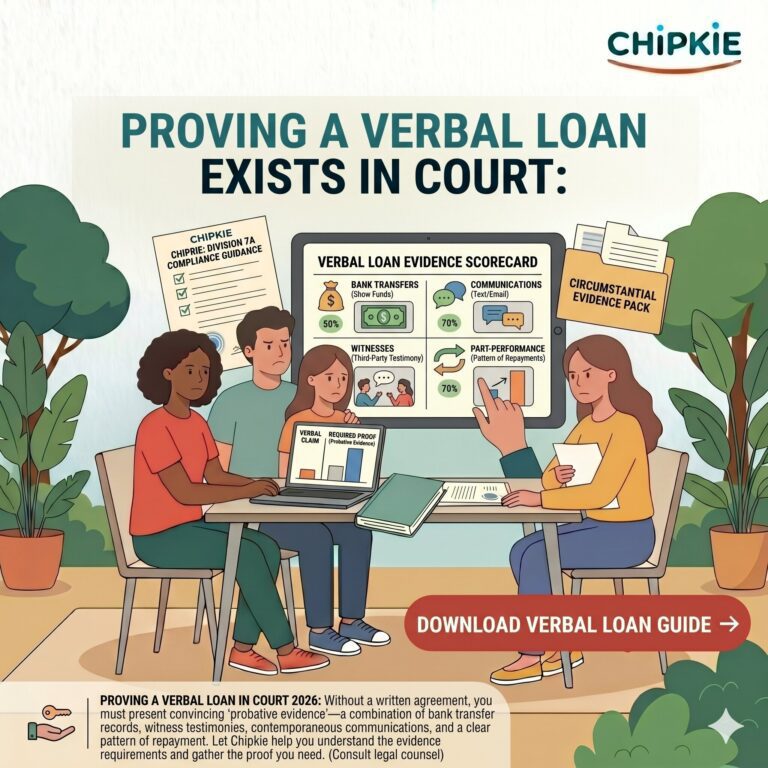

What evidence do courts accept when proving a verbal family loan?

Courts accept any admissible evidence that demonstrates, on the balance of probabilities, that both parties understood the money was a loan. The strongest cases combine multiple types of evidence: bank records showing the transfer, written communications referencing repayment, witness testimony, and any partial repayments already made by the borrower.

Here is what judges typically weigh:

- Bank statements and transfer records: These prove money changed hands, though not the terms. A clear reference line (e.g., “loan to Sarah — repay by Dec 2025”) is surprisingly powerful.

- Text messages, emails, and WhatsApp conversations: Any message where the borrower acknowledges the debt, discusses repayment, or uses the word “loan” or “pay you back” is admissible and often decisive.

- Witness evidence: A third party who was present when the agreement was made can give oral testimony. Courts prefer independent witnesses over other family members, but any corroboration helps.

- Partial repayments: If the borrower made any payments back — even small or irregular ones — this strongly implies a loan rather than a gift.

- Contemporaneous notes: A diary entry, letter, or note made at or near the time of the agreement carries more weight than something drafted after the dispute arose.

- Conduct of the parties: Did the borrower ever thank the lender “for the loan”? Did the lender chase repayment before the relationship deteriorated? Patterns of behaviour matter.

One critical point our experience shows people routinely overlook: HMRC correspondence can be relevant too. If either party declared the transfer as a loan (for example, on a mortgage application or in a tax return), that declaration is admissible. Conversely, if the borrower told a mortgage lender the money was a gift, the lender in your family dispute will have a very difficult time arguing otherwise. The HMRC personal tax guidance explains how family money transfers interact with tax obligations.

What are the biggest obstacles to winning a verbal loan claim in court?

The single biggest obstacle is the legal presumption that applies specifically to family transactions. In cases between close relatives, courts may apply the presumption of advancement — the assumption that a transfer from parent to child, for example, was intended as a gift. While this presumption has been weakened by modern case law, it has not been abolished, and it shifts the evidential burden onto the person claiming the money was a loan.

Other common obstacles include:

- Contradictory evidence: If you told a solicitor, mortgage broker, or HMRC that the money was a gift, your claim is severely undermined — and potentially fraudulent if you signed a gifted deposit declaration.

- Vague or missing terms: If there was no discussion about when or how the money would be repaid, courts may conclude there was no genuine loan agreement at all.

- Destroyed or deleted messages: Courts can draw adverse inferences if a party has deleted relevant messages, but the evidence is still gone.

- Family loyalty: Witnesses who are themselves family members may be treated as less reliable, and some may refuse to testify at all.

- Disproportionate costs: In the County Court Small Claims Track (claims up to £10,000), legal costs are generally not recoverable, meaning a £5,000 claim could cost more to pursue than it is worth.

It is also worth understanding that even if you win, enforcement is a separate battle. A court judgment is not the same as money in your account. If the borrower has no assets or income, you may hold a judgment you cannot enforce — a situation the MoneyHelper service warns about frequently.

How can you strengthen your position before going to court?

Before issuing a claim, take practical steps to build and preserve your evidence. Even after the loan has been made verbally, you can significantly improve your legal position without the borrower’s active cooperation — and ideally with it.

- Send a written demand for repayment: A clear letter or email stating the amount lent, the date, and requesting repayment by a specific deadline creates a contemporaneous record. If the borrower replies without denying the loan existed, that response is powerful evidence.

- Preserve all communications: Screenshot and back up every text, WhatsApp message, voicemail, and email that references the money. Store them outside your phone in case of device loss.

- Request a retrospective written agreement: It is never too late to put a verbal loan in writing. Even a simple email exchange confirming the original terms, signed by both parties, converts your verbal agreement into documentary evidence. Our guide on how to write a family loan agreement in the UK explains how to do this properly.

- Consider mediation first: Courts expect parties to attempt alternative dispute resolution before litigation. Mediation is cheaper, faster, and preserves family relationships far better than a courtroom.

- Keep a timeline: Document every relevant date — when the money was lent, any discussions about repayment, any partial payments received, and when you first demanded repayment formally.

If the amount exceeds £10,000, consider instructing a solicitor. For smaller sums, the Small Claims Court is designed for litigants in person, and the Financial Conduct Authority provides general guidance on financial disputes, though note that private family loans do not fall within the FCA’s regulatory perimeter.

Does the presumption of advancement still apply in 2025?

The presumption of advancement — that transfers from parent to child are gifts — still exists in English law, though courts apply it with decreasing force. Section 199 of the Equality Act 2010, which would have abolished it, has never been brought into force. Judges now treat it as a weak starting point, easily rebutted by evidence of loan intent.

Can a text message count as a written loan agreement?

A text message can serve as evidence of a loan’s existence, but it is not typically a formal written agreement. However, if both parties exchanged messages setting out the amount, repayment terms, and mutual agreement, courts may treat those messages as equivalent to a written contract. The more specific the messages, the stronger the evidence.

What happens if the borrower claims the money was a gift?

The burden of proof shifts to the lender to demonstrate, on the balance of probabilities, that the transfer was a loan. If you cannot produce corroborating evidence — bank references, messages, witnesses, or partial repayments — the court may accept the borrower’s version. This is precisely why putting family loans in writing from the start is so important.

Is it worth going to court over a small verbal family loan?

For claims under £10,000, the Small Claims Track keeps costs low — court fees range from £35 to £455 depending on the amount. However, you cannot recover solicitor fees, and enforcement after judgment can be difficult. Weigh the amount owed against the potential cost to both your finances and your family relationship before proceeding.

Does a verbal loan carry a six-year or twelve-year limitation period?

A verbal loan agreement is a simple contract, subject to a six-year limitation period under the Limitation Act 1980. If the loan had been executed as a deed — a formal document signed, witnessed, and delivered — the limitation period would be twelve years. This is one of the strongest practical reasons to formalise any significant family loan as a deed.

What should you do right now to protect yourself?

Whether you have already lent money on a handshake or are about to, the single most effective step is to create a written record. Proving a verbal family loan in court is possible, but it is expensive, emotionally draining, and uncertain. A clear, signed agreement — even a simple one created after the fact — transforms your position from “my word against theirs” to “here is the document.”

Chipkie makes it straightforward to create a proper family loan agreement that covers the amount, repayment schedule, interest (if any), and what happens if circumstances change. Protect your money and your relationship — document the loan today, so you never have to prove it in court tomorrow.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered financial or legal advice. Property and lending laws in the United Kingdom vary and may change over time. We always recommend consulting with a qualified solicitor and mortgage broker before entering into a property purchase or financial arrangement with another party.