Buy Now Pay Later Loan Agreement Guide 2025

Understand what’s in your buy now pay later loan agreement, including 2025 law changes and how they affect Aussie consumers. See what you need to know.

Understand what’s in your buy now pay later loan agreement, including 2025 law changes and how they affect Aussie consumers. See what you need to know.

Discover how to set a fair interest rate family loan 2026 that protects your money and your relationships as an Aussie lender. Find out how.

Discover how a cost of living family loan can help manage rising expenses, plus key tips to protect your finances and relationships. Find out more.

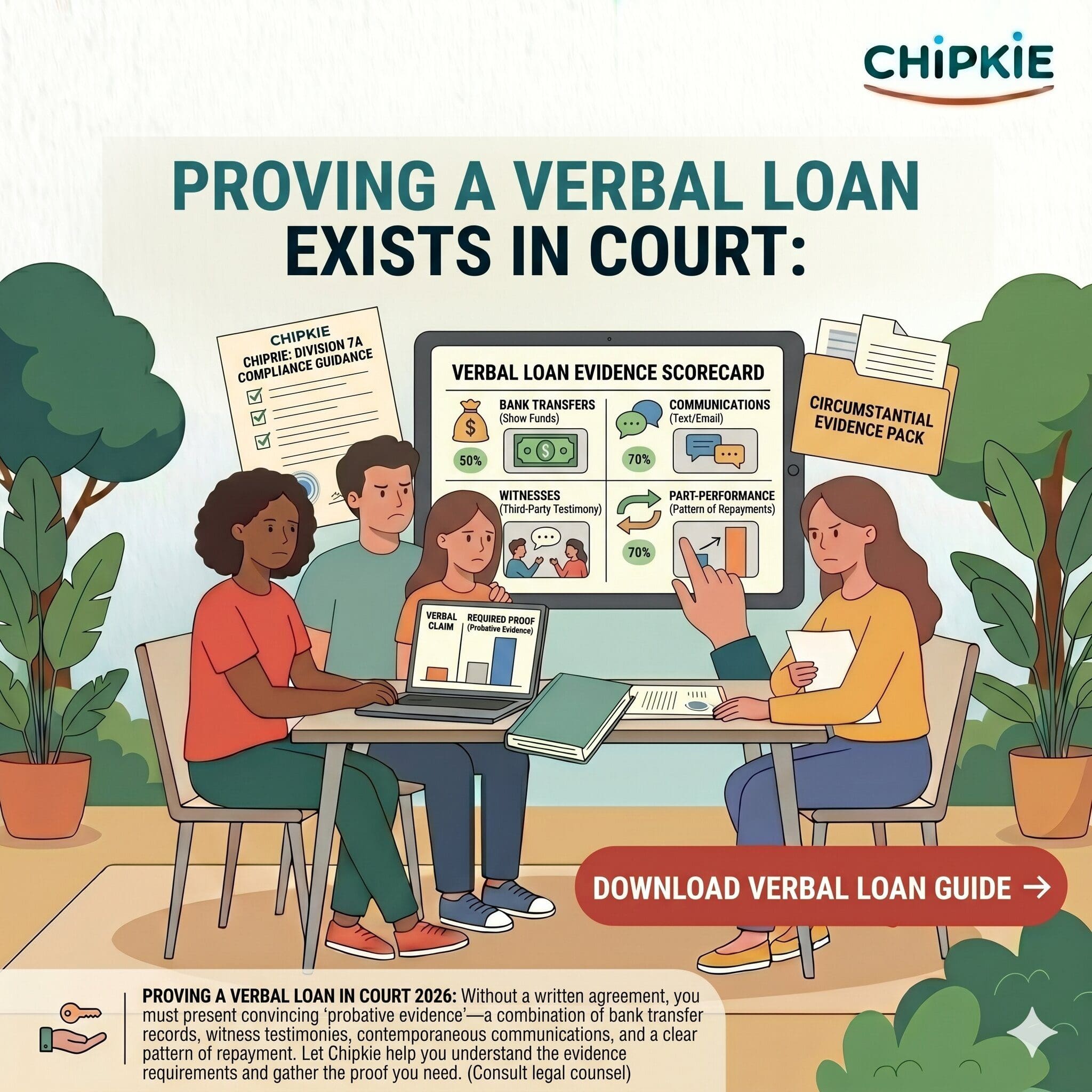

Discover what Australian courts demand when proving verbal family loan in court legal requirements, plus the evidence that strengthens your case. Find out how.

Discover how to ask family for emergency financial help safely without damaging relationships. Get practical tips for honest conversations. Find out how.

Discover the pawn shop loan risks borrowing from family instead could help you avoid, from sky-high interest rates to losing sentimental items for good.

Discover how the cost of living borrowing from family 2026 trend affects Aussie households. Learn the risks, tax traps, and practical tips to protect your finances and relationships.

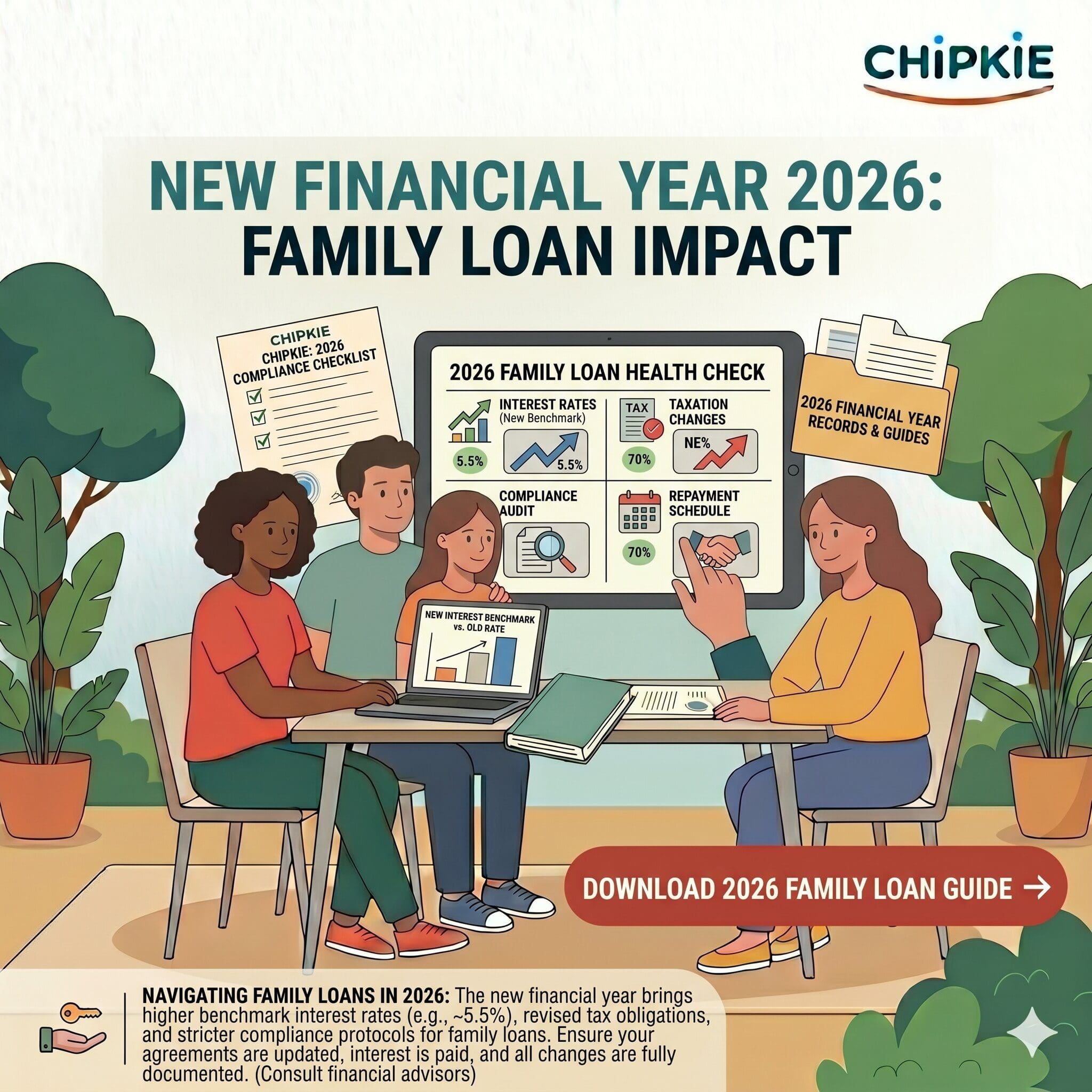

Discover how the new financial year 2026 family loan impact affects your tax, ATO compliance and private lending — essential tips for Aussie families.

Learn the steps for proving a verbal loan exists in court under Australian law. Discover what evidence you need, how courts assess disputes, and how to build a strong case.

Learn the Division 7A family loan agreement requirements to keep your company loans compliant and avoid costly deemed dividend assessments from the ATO.