In 2026, the Australian government threw former students a lifeline with a 20% reduction on all HELP/HECS loans. While this provided immediate relief, a fundamental problem remains for young Australians: student debt is a massive anchor on mortgage borrowing capacity.

When applying for a home loan, banks assess HECS debts harshly. A $30,000 student loan can reduce a first-home buyer’s borrowing power by significantly more than the debt itself.

This discrepancy has led to a massive trend in the “Bank of Mum and Dad”: parents paying off HECS debt in a lump sum just before the child applies for a mortgage to instantly boost their borrowing power.

It sounds like the perfect financial hack. But treating this payment as a casual “gift” is one of the most dangerous, wealth-destroying moves a parent can make.

The Divorce Black Hole

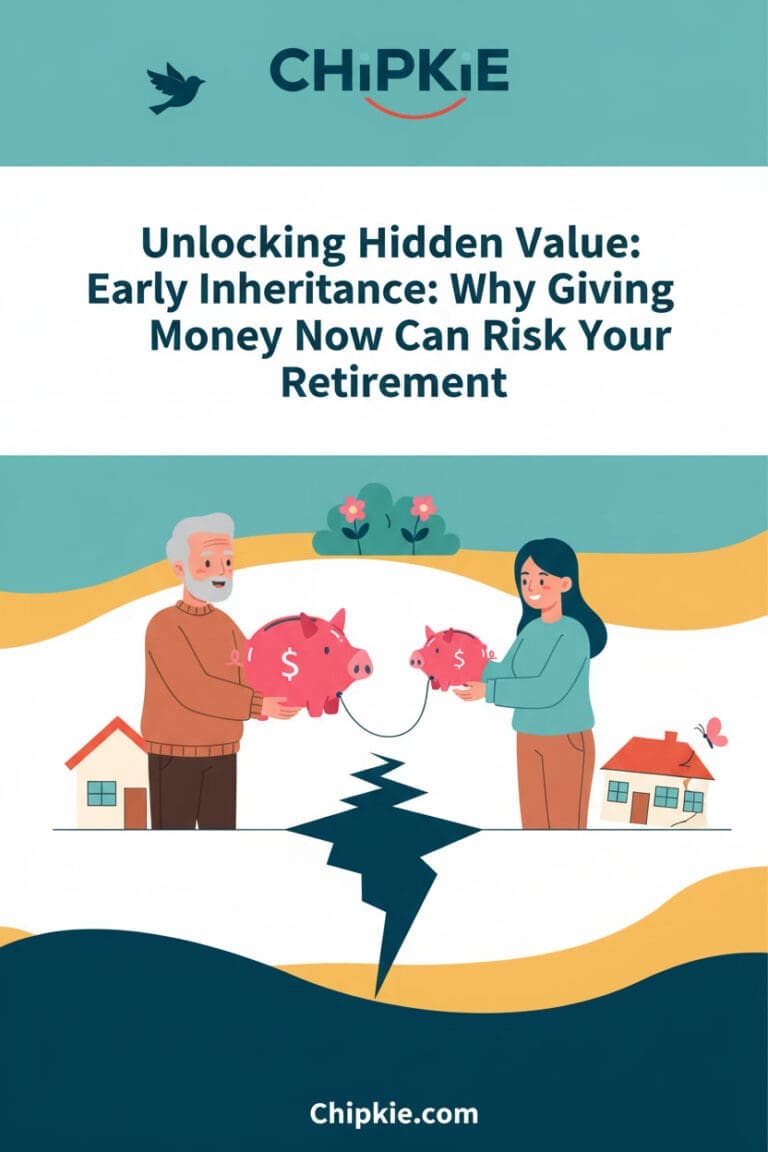

When you clear a child’s student loan with a cash gift, that money becomes legally untethered.

Let’s say you gift $40,000 to wipe the slate clean. Your child uses their newly boosted borrowing capacity to buy an apartment with their partner. Three years later, the relationship breaks down and they are forced to sell. Because your $40,000 was an undocumented gift that contributed to the couple’s overall wealth, it is absorbed into the marital asset pool.

The Family Court will likely split it, meaning you effectively just paid $20,000 toward your ex-in-law’s future. You can learn more about how a formal loan structure provides vital divorce protection here.

The Multi-Child Dilemma

The risks multiply when you look at the broader family dynamic. When you are managing the financial launchpad for four young adults navigating their late teens and early twenties, fairness is critical.

If you drop $40,000 to clear a university debt for the eldest so they can buy a house, what happens when the youngest decides to skip university entirely to start a business? Sibling resentment brews quickly when large, undocumented cash gifts are handed out unequally. Without a paper trail, there is no mechanism to balance these unequal gifts against future inheritances, often leading to bitter estate disputes decades down the line. To avoid the hidden tax and estate risks of unstructured handouts, it pays to understand the gift vs. loan tax trap.

The Solution: The “Loan Swap” Strategy

Smart families are abandoning the “gift” approach entirely. Instead, they are using platforms like Chipkie to execute a formal “Loan Swap.”

Here is how it protects your capital:

- You lend the money: You transfer the funds to clear the government debt, but you document it as a formal Family Loan.

- The Mortgage is Approved: With the government debt gone, your child qualifies for their home loan. (Note: You must disclose the family loan to the bank, but lenders often treat favourable family loans differently than rigid government tax debts).

- The Divorce Shield: Because your contribution is a registered legal debt, it is a liability. If your child divorces, your loan must be repaid before the property profits are split with the ex-partner.

- Estate Equalisation: If you pass away before the loan is repaid, the outstanding balance is simply deducted from that specific child’s share of the estate. The siblings are protected, and the math remains perfectly fair.

For a deeper dive into modernizing these agreements, check out our guide on how digital lending platforms are changing family loans.

🛡️ Protect the Bank of Mum and Dad

Paying off HECS debt is an incredible way to help your children enter the property market, but generosity requires a safety belt. Don’t rely on a handshake or a casual bank transfer. Use Chipkie to formalise the payment as a legally binding family loan. It ensures your child gets the house, your capital is protected from the Family Court, and your family relationships stay intact.

Disclaimer

Disclaimer: The information provided in this article is for informational purposes only and should not be considered financial, legal, or tax advice. Bank lending criteria and Family Law are subject to change. We always recommend consulting with a qualified mortgage broker and financial planner before making any financial decisions.