Lending money within a family is common—and usually informal. A handshake, a phone call, a promise over Thanksgiving dinner. But when repayment stalls and the relationship fractures, the lender faces a daunting question: how do you go about proving a verbal family loan in court when there is no written contract? Understanding the legal requirements for this process can mean the difference between recovering your money and walking away empty-handed.

Verbal agreements are, in most cases, legally enforceable contracts under U.S. law. The challenge isn’t legality—it’s proof. Courts won’t simply take your word for it. You need evidence, strategy, and an understanding of the rules that govern oral contracts in your state. This article walks you through every critical angle.

Are Verbal Loan Agreements Actually Enforceable in the United States?

Yes. Under the common law of every U.S. state, a verbal agreement to lend and repay money is a valid, binding contract as long as it meets the basic elements: offer, acceptance, consideration (the money itself), and mutual assent. No signature or written document is technically required for most personal loans.

That said, there are important exceptions. The Statute of Frauds—a legal doctrine adopted in some form by all 50 states—requires certain categories of contracts to be in writing. The most relevant one for family loans: agreements that cannot be performed within one year. If you lent your brother $40,000 with a verbal understanding that he’d repay it over three years, some courts may refuse to enforce that agreement because it falls outside the one-year window.

- Loans under one year to repay: Generally enforceable as verbal agreements.

- Loans over one year to repay: May be unenforceable under the Statute of Frauds, depending on state law.

- Loans involving real estate: Must almost always be in writing.

- Loans above a certain dollar amount: Some states (like California, under Civil Code § 1624) require writing for agreements exceeding a threshold.

Even when a verbal loan technically falls outside the Statute of Frauds, the practical problem remains: you have to prove the agreement existed. Judges and juries evaluate credibility, and “he said, she said” between family members is the weakest possible position.

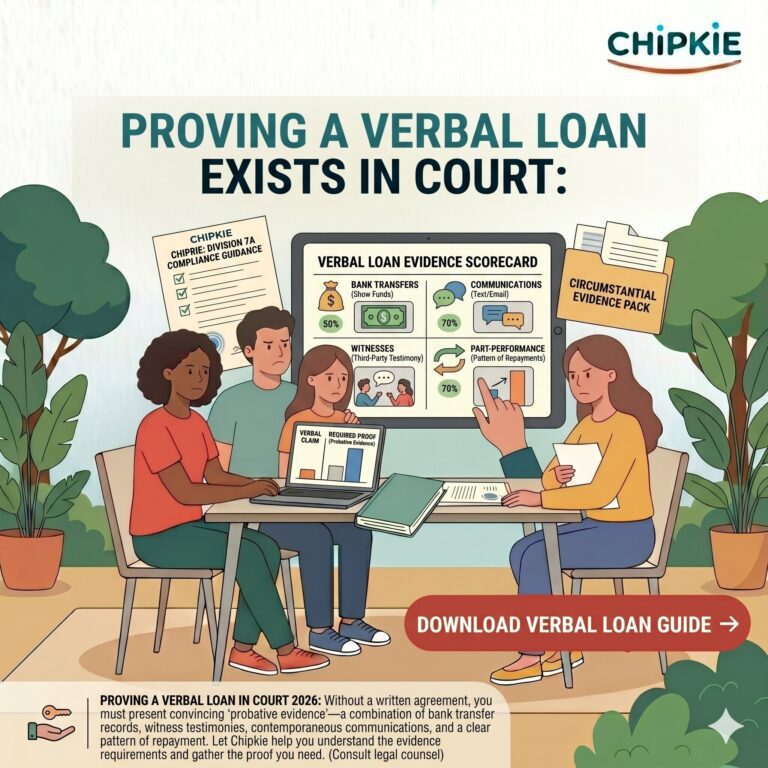

What Evidence Do Courts Accept to Prove a Verbal Family Loan?

Courts accept a wide range of circumstantial and documentary evidence to prove a verbal loan existed. You don’t need a single “smoking gun”—a pattern of consistent evidence is often more persuasive. The more types of proof you can present, the stronger your case.

Here are the categories of evidence that are most effective:

- Bank records and transfer receipts: A wire transfer, check image, Venmo transaction, or Zelle confirmation showing money moved from your account to the borrower’s account is foundational. Courts view this as near-irrefutable proof that a transfer occurred—though it doesn’t prove the transfer was a loan rather than a gift.

- Text messages, emails, and voicemails: Any communication where the borrower acknowledges the debt, discusses repayment terms, or references “paying you back” is powerful evidence. Screenshots should include timestamps, sender identification, and full conversation context.

- Partial repayments: If the borrower made even one payment, bank records showing an incoming transfer labeled “repayment,” “payback,” or even just from the borrower’s account on a schedule consistent with a loan are highly persuasive.

- Witness testimony: A third party—another family member, a friend—who was present when the loan was discussed or agreed upon can testify. However, courts often view family witness testimony with skepticism due to potential bias.

- Tax filings: If the loan was large enough that you charged interest and reported it to the IRS, your tax return itself becomes evidence of the loan’s existence. Conversely, if the IRS treated the transfer as a gift (because no interest was charged on a loan above the Applicable Federal Rate), that creates problems for your “loan” argument.

- Behavioral evidence: Courts also look at conduct. Did the borrower behave consistently with someone who owed a debt? Did they make excuses for delayed payments? Did they ask for extensions? This pattern of behavior implies an obligation.

The Consumer Financial Protection Bureau emphasizes the importance of documentation in all financial transactions. While their guidance typically addresses institutional lending, the same principle applies to family arrangements: if you can’t document it, you may not be able to prove it.

What Is the Biggest Legal Hurdle—and How Do Borrowers Fight Back?

The single biggest obstacle in proving a verbal family loan is the borrower’s almost inevitable defense: “It was a gift.” This is the default counter-argument in virtually every family loan dispute that reaches court, and it’s devastatingly effective when the lender has thin documentation.

Courts must determine intent at the time the money changed hands. Was it a loan (with an expectation of repayment) or a gift (freely given with no strings attached)? The burden of proof falls on the person claiming a loan exists—that’s you, the lender. Understanding how courts settle gift vs. loan disputes is essential preparation.

Factors courts typically weigh include:

- Was interest charged? Interest implies a commercial transaction, not a gift.

- Were specific repayment terms discussed? Even vague ones (“pay me back when you can”) suggest a loan.

- Was a due date set? A timeline signals obligation.

- What is the family’s history? If parents regularly give children money without expectation of return, a court may lean toward gift.

- Did the borrower’s financial situation suggest they needed a loan? Context matters—someone in financial distress is more likely to have borrowed than received a gift.

Another common defense is the statute of limitations. In most states, the clock for suing on a verbal contract is shorter than for written ones—often two to three years versus four to ten years for written agreements. In California, the statute of limitations on an oral contract is just two years (Code of Civil Procedure § 339), while a written contract gets four years. If you’ve waited too long, your claim may be time-barred regardless of the evidence you hold. Learn more about hidden statute of limitations rules for family loans before your window closes.

What Practical Steps Should You Take Right Now to Protect Yourself?

Whether you’ve already made a verbal loan or you’re about to, there are concrete actions you can take today to dramatically improve your legal position. Proving a verbal family loan in court becomes far more manageable when you build your evidence trail proactively.

- Send a confirmation text or email immediately after lending. Something as simple as “Just confirming the $5,000 I transferred today—let me know if the plan to repay by December still works” creates a timestamped record that establishes the transaction as a loan, not a gift.

- Use electronic payment methods, not cash. Cash is almost impossible to trace. Venmo, Zelle, checks, and wire transfers all create automatic records.

- Request partial payments on a schedule. Even $50 per month establishes a repayment pattern that courts recognize as evidence of a loan obligation.

- Keep every communication. Don’t delete texts, voicemails, or emails—even uncomfortable ones. A message from the borrower saying “I know I owe you, I just can’t pay right now” is worth more than almost any other piece of evidence.

- Put it in writing—even after the fact. It’s not too late to formalize a verbal agreement. A simple written note signed by both parties saying “This confirms the $10,000 loan made on [date], to be repaid by [date]” converts your verbal agreement into a written contract. Learn whether a DIY loan contract holds up in court—the answer is yes, in most circumstances.

- Consider IRS implications. For loans above $10,000, the IRS requires you to charge at least the Applicable Federal Rate (AFR) in interest. Failing to do so means the IRS may recharacterize the loan as a gift, which undermines your legal argument and may trigger gift tax reporting requirements.

How Much Can You Sue For Without a Lawyer?

If the loan amount is relatively small, small claims court is often the most practical venue. Every state sets its own small claims limit—ranging from $2,500 in some states to $25,000 in others (Tennessee allows up to $25,000; many states cap at $10,000). You don’t need an attorney, filing fees are typically $30–$100, and cases are resolved quickly.

| State | Small Claims Limit | Oral Contract Statute of Limitations |

|---|---|---|

| California | $12,500 | 2 years |

| Texas | $20,000 | 4 years |

| New York | $10,000 | 6 years |

| Florida | $8,000 | 4 years |

| Illinois | $10,000 | 5 years |

For amounts above the small claims threshold, you’ll likely need to file in civil court, where attorney fees can quickly exceed the amount you’re trying to recover. This is another reason why documentation matters so much—a well-documented case is more likely to settle before trial.

Can a Text Message Serve as a Written Agreement?

In many states, yes. Under the Uniform Electronic Transactions Act (adopted by 47 states and D.C.), electronic communications can satisfy the “writing” requirement of the Statute of Frauds if they contain essential terms—amount, parties, and intent to repay. A clear text exchange may function as a written contract.

What If the Borrower Denies the Conversation Ever Happened?

This is where corroborating evidence becomes critical. Bank transfer records prove money moved. Witness testimony places context around the transfer. Any subsequent communication—even the borrower’s silence in response to a repayment request—can be used. Courts evaluate the totality of evidence, not any single piece.

Does It Matter If the Loan Was Between Parent and Child?

Yes, it often does. Courts apply heightened scrutiny to parent-child financial transfers because gifts between parents and children are so common. The Federal Trade Commission notes that family financial disputes are among the most complex consumer issues. Parents lending to children should be especially diligent about documentation.

Can You Still Formalize a Verbal Loan Agreement After the Money Was Transferred?

Absolutely. Both parties can sign a written memorandum at any time acknowledging the loan’s existence, the amount, and repayment terms. This after-the-fact documentation converts the verbal agreement into a written one, which strengthens enforceability and extends the statute of limitations in most states.

Why Does This All Come Down to Documentation?

Every attorney who handles family loan disputes will tell you the same thing: the case is won or lost before anyone walks into a courtroom. The evidence you gather—or fail to gather—in the days and weeks after lending money determines your outcome years later. Verbal agreements are legal, but proving them is a different challenge entirely.

Don’t let a family loan become an unrecoverable loss or a relationship-destroying lawsuit. Chipkie helps you create clear, enforceable loan agreements, track repayments, and build the kind of documentation trail that protects both lender and borrower. Whether you’re lending $500 or $50,000, start with a written agreement—your future self will thank you.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered financial or legal advice. Laws and lending criteria vary significantly between states. We always recommend consulting with a qualified real estate attorney and financial advisor before entering into a property purchase or financial arrangement with another party.